In The Markets

The markets continue to prove everyone wrong. Despite ongoing calls for a stock market correction, global stocks had a very healthy quarter and have solid gains year-to-date. As you can see below, this is true for US large cap and small cap stocks, foreign stocks and emerging markets. US Large Cap Stocks led the way with gains of 5.23% for the quarter, and developed foreign markets weren’t far behind, up 4.09%. Bonds have also had a strong year so far in 2014, up 3.93% in 2014, much to the chagrin of nearly every market commentator and prognosticator who have been calling for a spike in interest rates. Not pictured are US REITs, up an astonishing 7.61% in the quarter and 17.79% year-to-date (Morningstar US Real Estate Index).

It has been nearly three years since the markets experienced any meaningful stock market correction (in fact we have gone 1,000 days without a 10% drop), and we have seen very little volatility this year in US markets. Below is a chart of the VIX, the measured daily volatility of the S&P 500, which seems to be in permanent decline.

For practically five years market commentators have also been telling us that bonds have “nowhere to go but down,” and they are still being proven wrong as bonds of all stripes are putting up positive numbers. This market environment (truly every market environment) should serve as an excellent reminder that no one can accurately predict what comes next. The future remains unknowable, and the economic, emotional and geopolitical forces that move markets are both plentiful and much too complicated to be predicted. While some may say we are “due for a correction” the fact is that the market listens to no (wo)man and doesn’t care too much about what lines you care to draw on a chart. We will, someday, have a market correction and another bear market but it certainly won’t be because someone on CNBC said we are “due.”

In The Economy

Economic data presented in the first half of this year has varied widely. There was a sharp drawdown in economic activity in the first quarter as GDP dropped -2.9% year-over-year. Since then, we have seen a large increase in real estate activity and home values. New single-family home sales have been on the rise for a few years:

And national home prices are on the upswing as well:

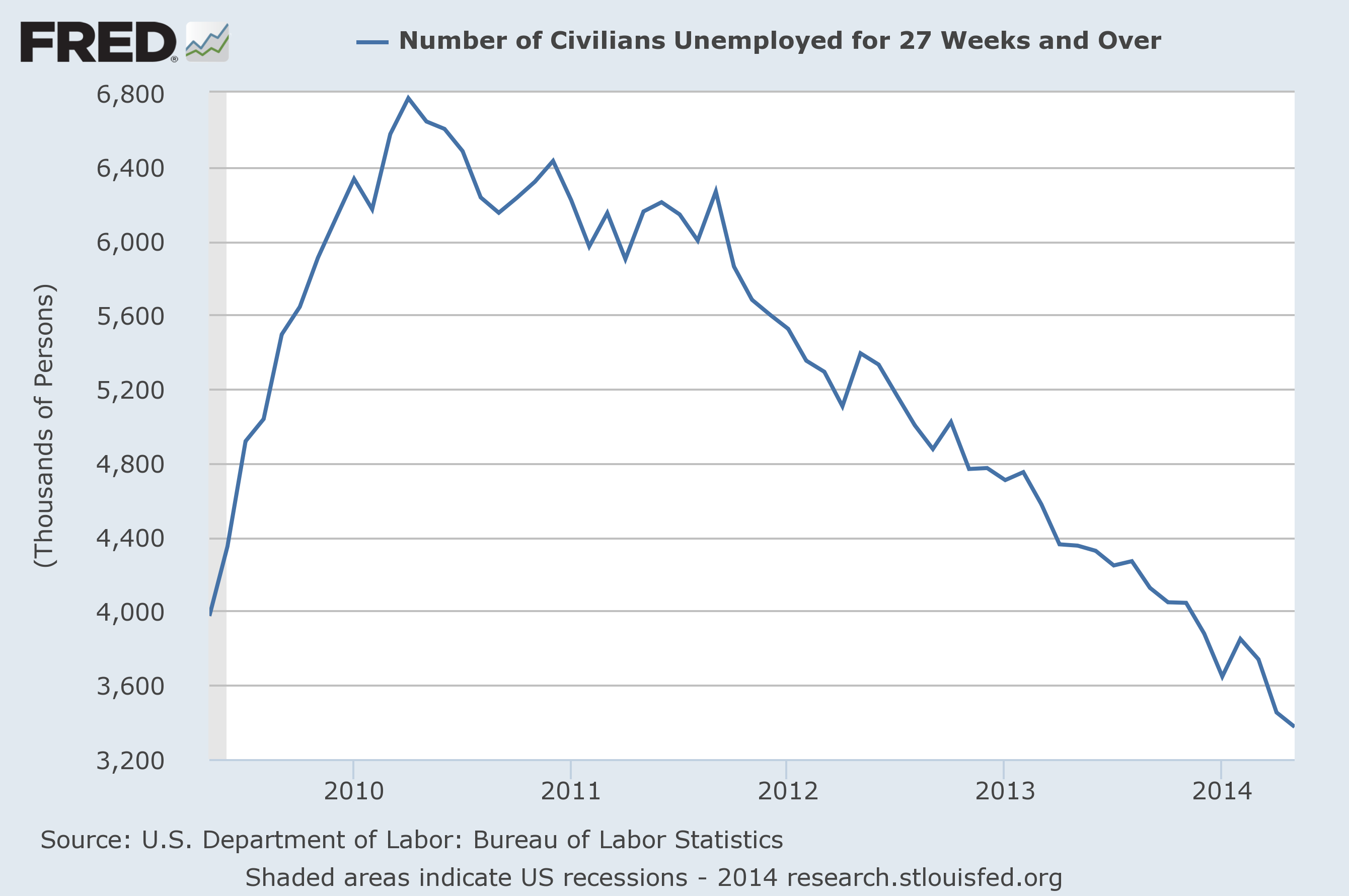

Job reports have also been encouraging as new unemployment claims remain just above 300,000 and unemployment has fallen to 6.3%. The ranks of the long-term unemployed have shrunk to 34.6% of total unemployment from 37.4% a year ago and new job openings are approaching their highest level since March 2007 with the most recent report of 4.5 million openings in April, up from 4.2 million this March.

The general economic trend remains positive but muted, as it has for several years. What comes next is anyone’s guess, and what we have recently seen is typical this far into a recovery as labor sees improvement, asset prices continue to gain and we see the very beginnings of inflation.

In Washington

There has not been much activity out of Washington this year. For better or worse, the current 113th Congress has passed a very small amount of legislation. Unfortunately, this includes extending several popular tax breaks that expired at the end of last year. Notably, this list includes the very popular tax-free charitable retirement account distribution that had been in place for the past several years. While it is possible that the legislation will still be passed later this year, for now we will have to wait and see.

During his 2014 State of the Union, President Obama announced his desire for a new retirement account, the MyRA. Intentionally designed for individuals without access to a workplace retirement plan, the MyRA would allow individuals to invest for retirement in a Treasury bond. Accounts can be funded annually until the account balance reaches $15,000, at which time the funds can be moved to a Roth IRA. It is clear with the lower maximum account value limit and limited investment options that this plan is designed for lower income individuals who may not otherwise save. Other than ease of use (via a payroll deposit) the plan has no significant advantages over a Roth IRA, which has more flexible investment options and higher contribution limits. This might be a good step to make things easier for lower income individuals to save, but I still feel that a better fix for the current mess of our retirement system would be to simply open access to the Thrift Savings Plan to all Americans via payroll deposits.

As always, I will not pretend to anticipate the future of the economy or the markets. Successful investors will control their costs, taxes and behavior and leave the speculating for the racetrack.

(Index returns as follows: Large Cap US Stocks – S&P 500; Small Cap US Stocks – Russell 2000; Foreign Developed Markets – MSCI EAFE; Emerging Markets – MSCI EM)