Every time we have a release of economic data, people seem shocked by the underlying trend. Recently it’s been falling unemployment (by any measure) and upward pressure on wage growth. We shouldn’t be surprised – this is, in fact, exactly what we should expect to see in this point of an economic cycle.

Here’s where it begins. Let’s say it is 2007 and the broad economy is about to peak. Recession is around the corner. What’s happening?

– Asset prices are peaking. Stocks, houses, etc. Probably bottles of wine, but I don’t have a great index for that.

– Business investment is slowing. Revenue growth is slowing. Nobody gets a raise.

Then what happens? Recession hits (I’m not going to even try to touch they “why” here. There’s no consensus. Safe to say, recessions happen). Stocks fall off of their highs. The layoffs begin. Unemployment is starting to tick up, jobless claims are on the rise.

Now it’s the end of ’08, early ’09. Peak recession. Layoffs are skyrocketing. Unemployment is nasty. Asset prices are in the toliet. Warren Buffet is writing an op-ed that these things are temporary, everyone is calling him an old kook. Previously thought to be untouchable public companies are going bankrupt. Junk bond issuers are defaulting.

The first “green shoots” come from the stock market. It bottoms. Markets are forward looking – there’s no bell rung at the bottom, but investors are starting to wonder if maybe this isn’t the apocalypse after all. Stock prices start to tick up. Headlines abound screaming about “dead cat bounces” and “knife catching value investors.” The economy is still nasty. No one is getting a job. Don’t even think about asking for a raise. Why would you get a raise? There are 20 people lined up outside asking to do your job for 70% of the pay.

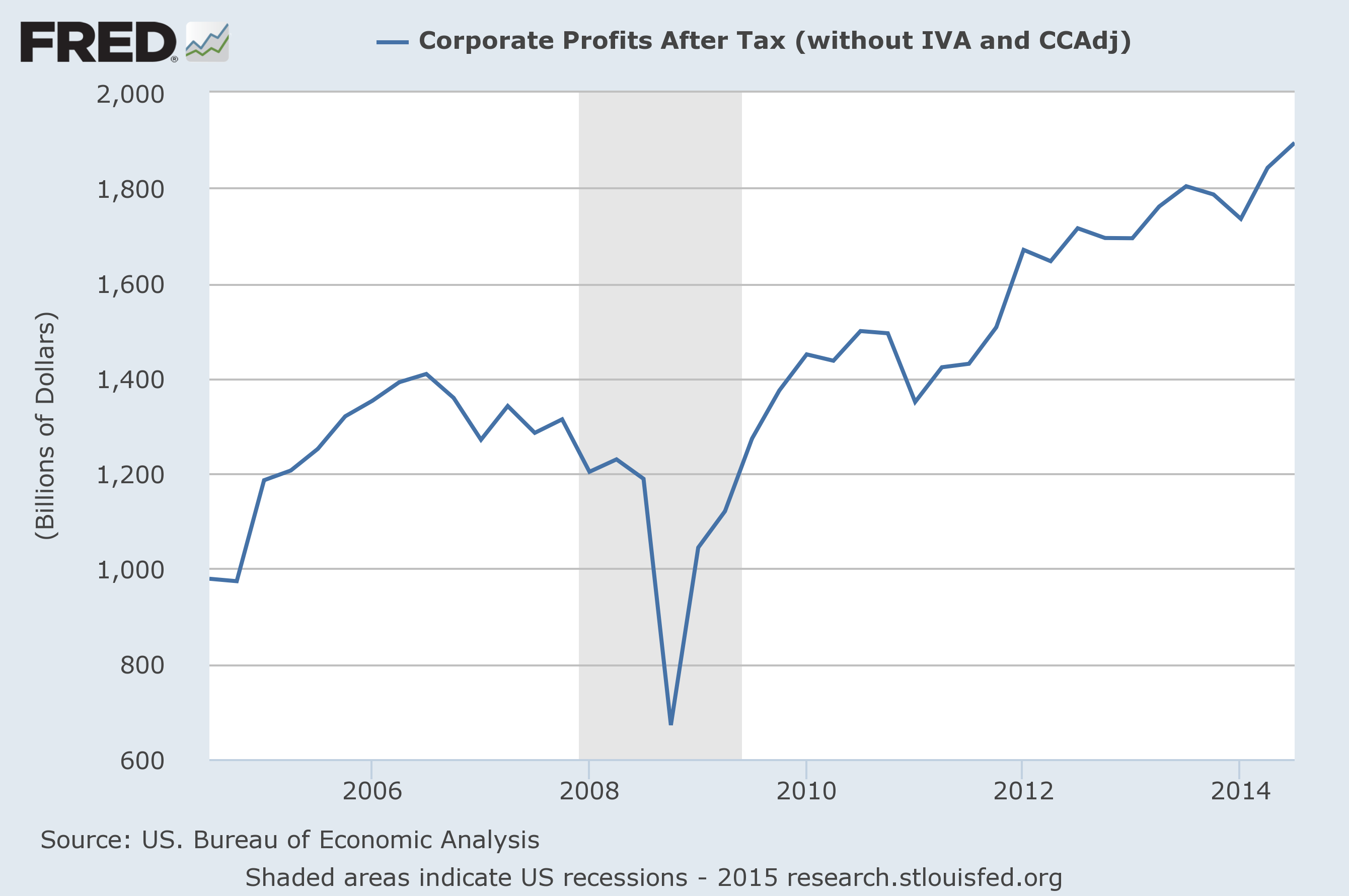

The market recovery seems to be taking hold. But is it real? Corporate profits were horrible last year – why is this year going to be so different? But then it starts to happen. Corporate revenues stabilize. Because of widespread cost cutting, profits jump. Markets tick up a bit higher. Naysayers holler that this isn’t a “real” recovery because there is no revenue growth.

And then, just like that, there’s revenue growth. For many sectors it’s not exciting, but it’s moving in the right direction. Profit margins are expanding at a breakneck pace thanks to recession-era levels of overhead. There isn’t a lot of reinvestment yet – corporate America is stomping on the stone, looking for a bit more blood before they are forced to increase spending. Remember – this is what corporations are trying to do – maximize profits. They increase capital investment, hiring and spending when they need to, not out of the generosity of their warm hearts.

Right about now is when you read 1,000 stories about the “jobless recovery.” Guess what? Every recovery starts out as a jobless recovery.

Then, a guy running a widget factory realizes that if he wants to keep selling more widgets, he is going to have to grow. He needs a few more sales staff and a few more factory workers and maybe replace that old machine he has been limping along with for the last four years. He believes that the growth is sustainable so he starts spending some money.

And so unemployment starts to slow down. Initial claims are dropping. The rate is growing slower, maybe leveling off. Business start to invest in people, machines, technology, advertising.

You still can’t get a raise yet, because there are still 15 people lined up outside who want your job.

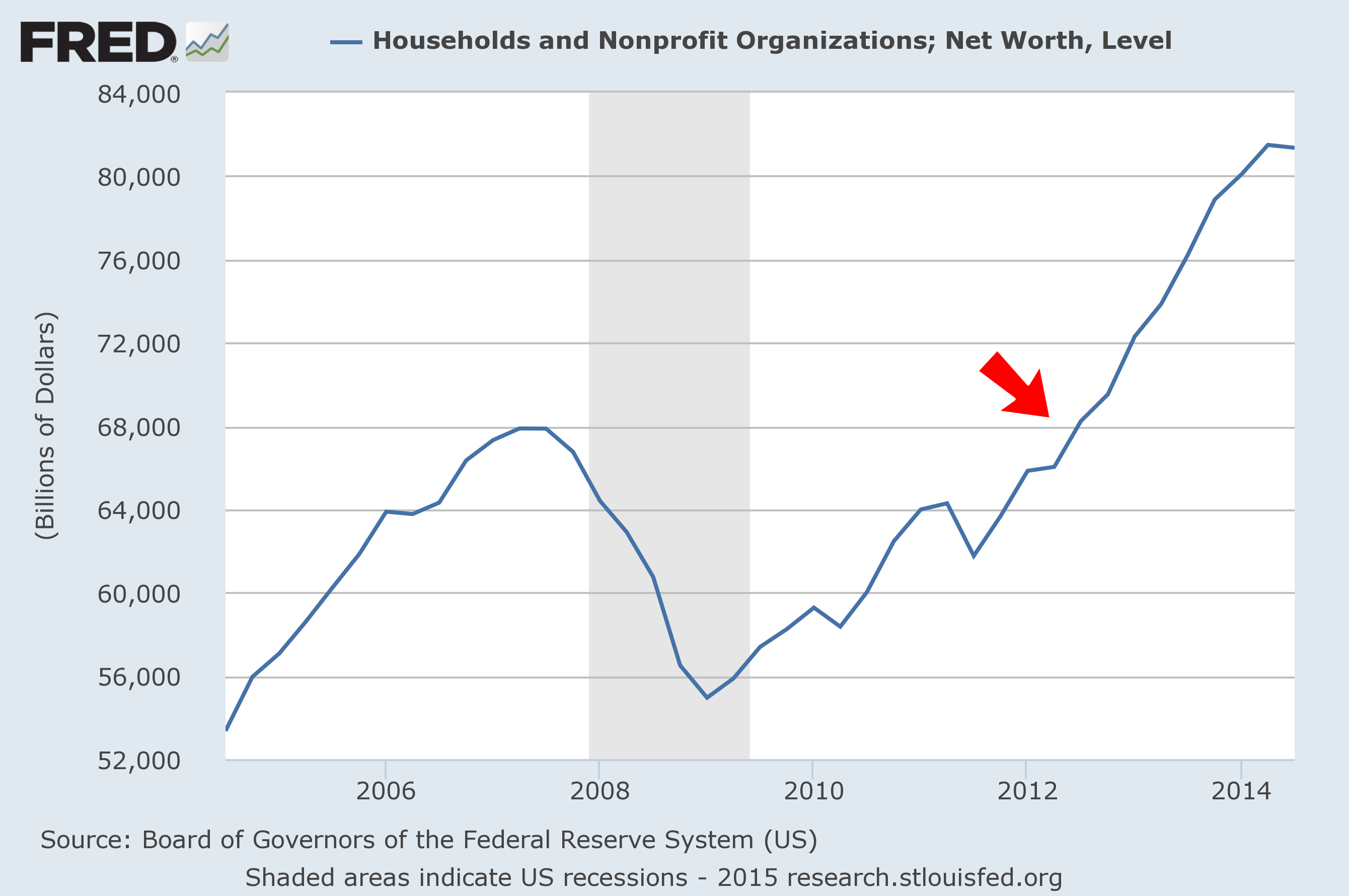

And along we go. Corporate profits are pretty healthy, the stock market has probably recovered by now. Unemployment is officially trending down. Consumers take a deep breath and relax. Balance sheets, both corporate and household, are looking better than they did a few years ago. It’s definitely not the apocalypse. Everybody spends a little more at Christmas. You finally take that vacation or replace the family car.

Consumer spending and business investment drive more corporate revenue growth. Some sectors are really taking off now. Unemployment has fallen nearly to pre-recession levels. Initial jobless claims reach a post-recession low. Now instead of “jobless recovery” headlines we see stories about how the average household hasn’t seen a raise in real terms in years.

But with unemployment falling, the number of qualified applicants for your job is getting small. In fact, a recruiter called you last week about another opportunity. Maybe you’ll quit! The balance of power begins to shift from the corporation to the employee. More people start quitting their jobs. More people are getting raises, they are getting more working hours per week. People who left the workforce are coming back. And wage pressures rise. Employers give in to keep good people. 401(k) matches get a boost, bonuses are back. In-demand sectors have bidding wars over talent, or simply buy their competitors for talent. Then we are bewildered by a headline that the nation’s largest retailer is boosting wages for its lowest paid workers.

And here we are. Asset prices are reaching new highs. Unemployment is trending near average levels. Initial jobless claims have been very low. Corporate profits are steady, but we’re aware that labor costs could begin to have an impact. Households are borrowing again, to buy new cars and homes. Residential and commercial construction is booming again. Wal-Mart, the Gap, TJ Maxx and Marshalls have all recently announced significant wage increases for hourly workers. This morning’s announcement was that consumer spending grew a 4.2% in the fourth quarter, the fastest annual rate since 2006. And yet, some among us are surprised to find us here.

The fact is that eventually we’ll have another recession. Stock markets will fall. People will lose their jobs. Businesses that were squeaking by will fail. Individuals and businesses will file for bankruptcy. Bond issuers will default. Consumer discretionary spending will slow. I’m not one for predictions, but I would make a reasonable bet that when the cycle starts again, it won’t look too different from 30,000 feet.

{kind=link}